https://commercial-appraisers.com/wp-content/uploads/2013/07/Spreadsheet-Photo.jpg

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

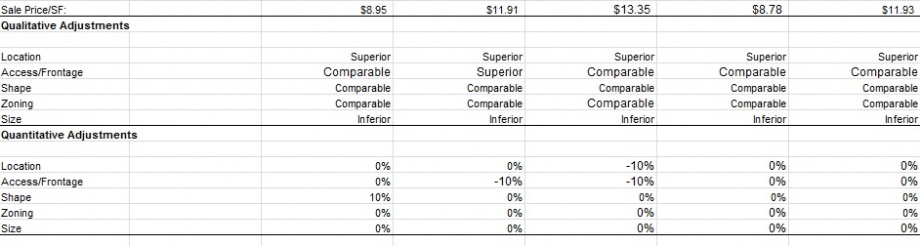

chrisrolly2013-07-23 15:35:262026-01-18 21:08:43Quantitative vs. Qualitative Adjustments

https://commercial-appraisers.com/wp-content/uploads/2013/07/Spreadsheet-Photo.jpg

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-23 15:35:262026-01-18 21:08:43Quantitative vs. Qualitative Adjustments https://commercial-appraisers.com/wp-content/uploads/2013/07/P5080015.JPG

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-22 19:51:562026-01-18 21:06:23The Unfinished Office Park

https://commercial-appraisers.com/wp-content/uploads/2013/07/P5080015.JPG

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-22 19:51:562026-01-18 21:06:23The Unfinished Office Park https://commercial-appraisers.com/wp-content/uploads/2013/07/P1010048.JPG

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-19 17:53:442026-01-18 21:12:19The Religious Facility Appraisal – Part IV

https://commercial-appraisers.com/wp-content/uploads/2013/07/P1010048.JPG

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-19 17:53:442026-01-18 21:12:19The Religious Facility Appraisal – Part IV https://commercial-appraisers.com/wp-content/uploads/2013/07/pics-003.jpg

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-18 13:42:222026-01-18 21:14:30The Religious Facility Appraisal – Part III

https://commercial-appraisers.com/wp-content/uploads/2013/07/pics-003.jpg

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-18 13:42:222026-01-18 21:14:30The Religious Facility Appraisal – Part III https://commercial-appraisers.com/wp-content/uploads/2013/07/Picture-022.jpg

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-17 18:56:462026-01-18 21:15:18The Religious Facility Appraisal – Part II

https://commercial-appraisers.com/wp-content/uploads/2013/07/Picture-022.jpg

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-17 18:56:462026-01-18 21:15:18The Religious Facility Appraisal – Part II https://commercial-appraisers.com/wp-content/uploads/2013/07/P7080048.JPG

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-12 13:18:372026-01-18 21:15:56The Religious Facility Appraisal – Part I

https://commercial-appraisers.com/wp-content/uploads/2013/07/P7080048.JPG

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-12 13:18:372026-01-18 21:15:56The Religious Facility Appraisal – Part I https://commercial-appraisers.com/wp-content/uploads/2013/07/flhouse1.jpg

1001

1500

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-10 21:33:452026-01-25 03:23:14Florida State Homes Article

https://commercial-appraisers.com/wp-content/uploads/2013/07/flhouse1.jpg

1001

1500

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-10 21:33:452026-01-25 03:23:14Florida State Homes Article https://commercial-appraisers.com/wp-content/uploads/2013/07/Aerial.jpg

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-10 14:22:452026-01-18 21:19:40A common mistake – What to do with “extra” land

https://commercial-appraisers.com/wp-content/uploads/2013/07/Aerial.jpg

246

920

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-10 14:22:452026-01-18 21:19:40A common mistake – What to do with “extra” land https://commercial-appraisers.com/wp-content/uploads/2013/07/Narrative-Appraisal-Report.png

1031

1200

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-09 19:14:532026-01-25 03:31:21Commercial Appraisal Report Format Changes For 2014

https://commercial-appraisers.com/wp-content/uploads/2013/07/Narrative-Appraisal-Report.png

1031

1200

chrisrolly

https://commercial-appraisers.com/wp-content/uploads/2018/08/CIA-Logo-3.png

chrisrolly2013-07-09 19:14:532026-01-25 03:31:21Commercial Appraisal Report Format Changes For 2014